Work are changing schemes and want suggestions for which one they go with. Anyone know any details of which is the best one or pros and cons of the different providers?

Currently evanscycles (which are accepted at other places) and limit of £1k.

Already asked for limit to be raised to at least £3k

It’s not going to answer your question really, but we use cyclescheme, and the limit was increased to £10K a few years ago, so that e-bikes could be purchased rather than a lot of professors riding around on Pinarello’s!

Some places will accept Cycle scheme on sale price items. Evans being one.

Many places now charge 10% commission on CTW as that’s what they lose on the voucher.

I agree with a lot of what Poet says. It is definitely less attractive since the VAT relief that many got in the early years was lost. That’s been the known position for a long time now though.

I disagree with this bit. None of my salary sacrifices impact my pension, so it will be company by company. We can salary sacrifice for extra holiday, etc. My pension is still based off my stated base salary in the system.

Not saying a company couldn’t operate it that way, but it’s definitely not a given.

It’s not really a question about whether I’m going to use it right now but if you had to pick a scheme which would it be.

Some places say no sale bikes but some will. Some charge an extra fee to cover scheme admin costs, some don’t.

Also, when’s the last time you saw a bike genuinely on sale? I can get 25% off specialized but they have 0 stock of road bikes on their website once you get past the entry level models.

Probably one that offers the option of not charging and admin fee

One that will offer a supplier who actually has bikes in stock at the price range potential employees will want to purchase at - maybe look at doing a quick poll at work?

Are bike to work schemes more attractive if you’re in the higher tax brackets?

I have no idea about tax efficiency, but I suspect I’m not efficient because I don’t know what the fuck I’m doing and I’m too exhausted all the time to think about it.

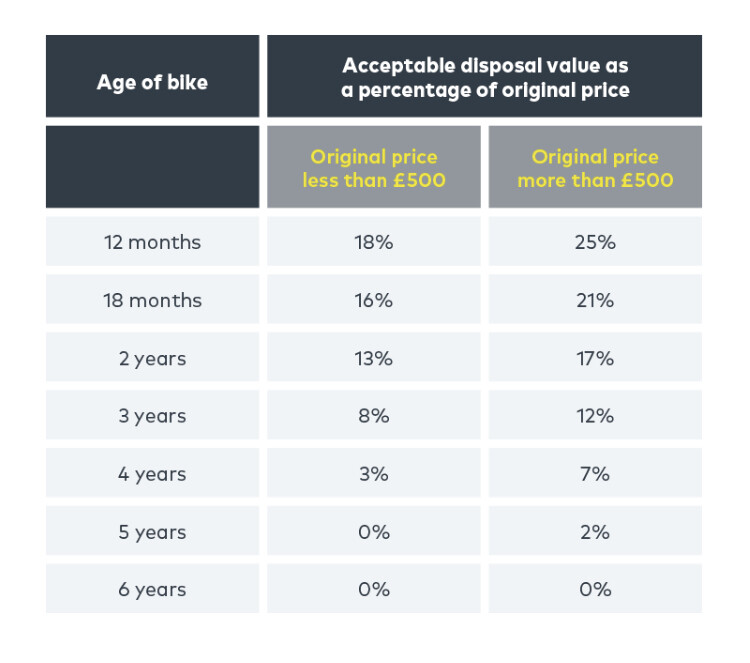

Coincidentally this morning my 5 year statement came through from Evans. This is the table from the email.

The 1 year transfer value is where you got the 25% from yes? As you can see, this reduces to 0% over 6 years.

What matters is when you leave the employer that is providing the loan, and the percentages you get charged what stage. So if I leave then I’m charged larger sums unless I stay there forever.

So I spoke to my employer about what happens if I leave after the first 12 months, they said it’s nothing to do with them, speak to the bike shop. The bike shop say it’s nothing to do with them, speak to the employer.

It very much depends which scheme you use. My understanding of cyclescheme, as an example, is that they take over the “contract” after the employer salary deductions end. And so they administer the final balancing payment. I think they follow the rules fairly prescriptively. But some others are a bit more carefree.

It is on the whole a lot more regimented nowadays tho. Back in the day you saved the VAT too, but HMRC finally set some boundaries and participants in the schemes are expected to follow them